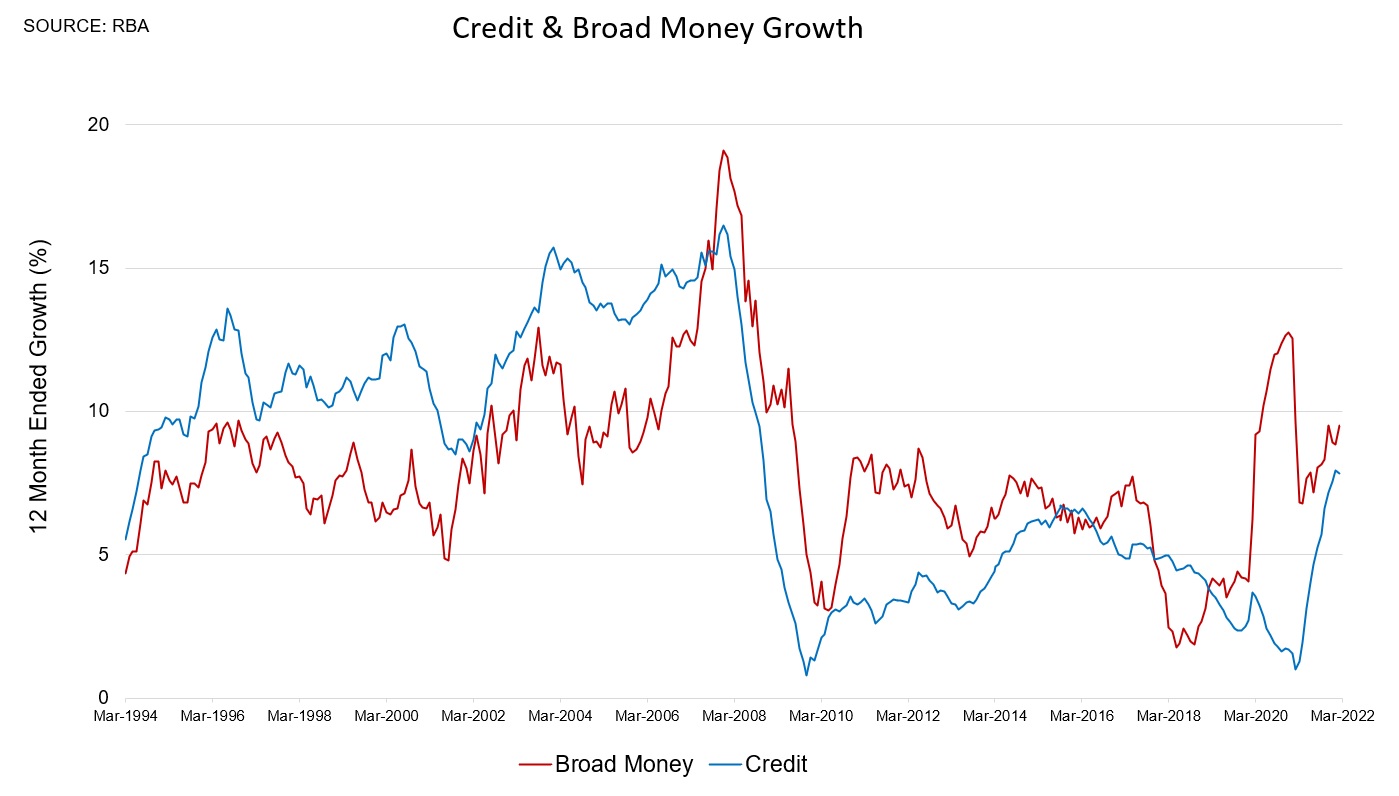

Credit growth eases

Credit growth in the Aussie economy slowed to 0.4 per cent in March, the slowest monthly growth in nearly a year, despite solid results for business and housing credit.

Owner-occupier credit growth is now slowing, and is being replaced by investors seeking an inflation hedge.

With the real cash rate deeply (!) in negative territory, investors will be looking for markets in which to deploy their excess savings, especially given the chronic shortage of rental properties leading to surging rents.

Despite the return of investors, overall housing credit growth looks to be peaking out.

And indeed the housing credit impulse shows that the peak of annual price growth has already long since passed for this cycle, with steadier results to be expected over the period ahead.

Construction costs soar

In other news, the producer price index figures followed a similar trajectory to consumer prices, rising by 4.9 per cent over the year.

As earlier implied by the ABS, there were some major increases in materials costs.

Input construction costs for houses were up by more than 15 per cent over the year (17 per cent in Melbourne), driven by sharp increases in the price of timber and other metals.

Output costs across all construction sectors increased at a double-digit pace for the first time since the data series began in 1996.

I recently discussed this dynamic with some developers at an event in Queensland.

Their view was that supply chains may well right themselves in time, but typically prices tend to be sticky and construction costs are unlikely to come back down by much, if at all.

If they prove to be correct, this suggests further developer insolvencies ahead - and an undersupply of dwellings - with the cost of building a new home gapping irreversibly higher.