Retail slowdown

It's been a rollercoaster journey for retail sales over the past couple of years, spurred higher by the stimulus and the inability of Aussies to travel overseas, yet intermittently disturbed by lockdowns.

Online retail in particular has really been pumping.

Anecdotally, a great many Aussies are currently travelling or visiting Europe, and the June retail figures were weak, recording only a 0.2 per cent increase in nominal terms.

Given prices have been rising, this was effectively a negative result, with food, department stores, and household goods retail turnover all dropping.

The year-on-year figures still look strong, partly because of the base effect.

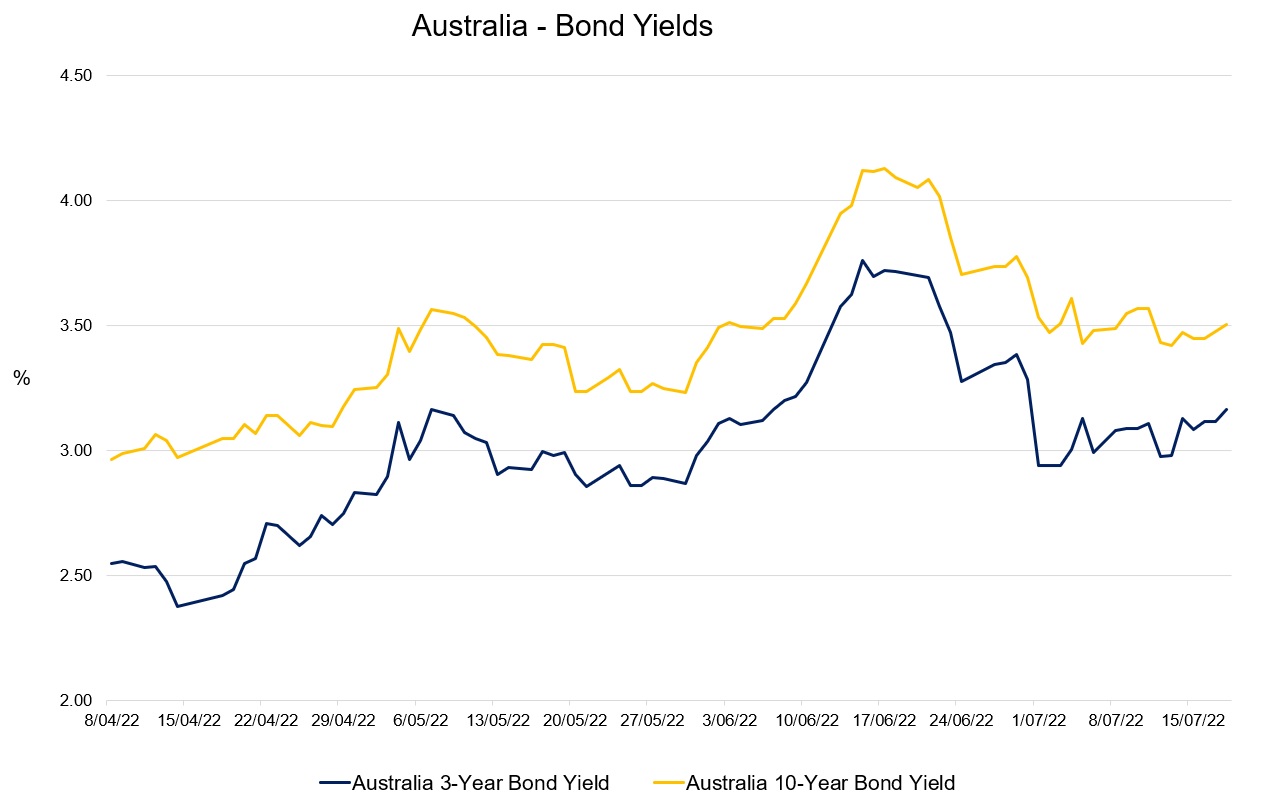

Overall, it seems that markets were fairly sanguine about this week's inflation figures - perhaps not quite as hot as markets secretly feared - and bond yields have eased all the way back down to where they came from in May, declining further on the latest news out of the U.S.

The US economy recorded a second consecutive quarter of negative growth according to the preliminary data, which is what they used to refer to as a r....well, anyway.

Markets thing inflation will ultimately peak, and then eventually head lower, with interest rates following suit (potentially starting with a cut as soon as Q1 2023, which seems quite remarkable, all things considered).

Commodities prices super-boom!

With the Fed moving to a meeting by meeting basis for the assessment of monetary policy, stock markets have been rather be enjoying this potential pivot over the past couple of days.

And in Australia?

Commodity prices are having an absolutely monster run, with Australia's export price index soaring to unprecedented highs, and the June quarter set to awesome record highs for the terms of trade.

This is a tremendous boost for government tax take and Australia's domestic income.

Iron ore export prices look to have peaked, but coal export prices continued to go vertical in the June quarter, while gas prices have also been running at extraordinarily high levels.

The ASX 200 has recovered a little in sympathy to 6,889, having pulled back to 6,433 in June.

Pulling in the other direction banks are likely to come under some significant pressure as lending has slowed.

Rewinding to early 2020, I'd previously felt on the balance of probabilities the ASX could be in for a tough time.

After the XJO first breached 7,000 I moved most of my liquid assets out of stocks (though obviously I still had some very long-term investments in index funds) and ended up buying a couple of investment properties in the 2020 panic instead.

But after the initial COVID crunch when the Aussie stock market very briefly fell to under 5,000, overall the decline for Aussie stocks has proved to be pretty tame and modest to date, to be fair.