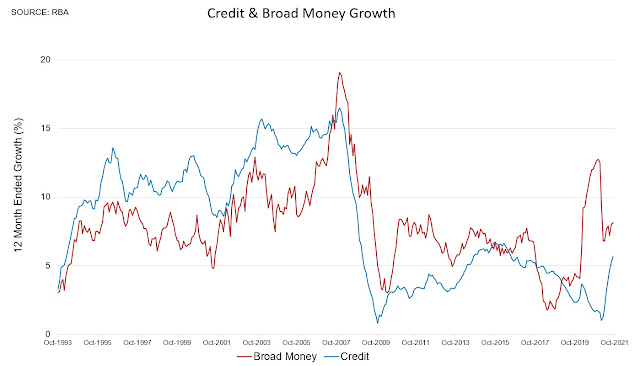

Housing hype

There's been some lively debate about whether the prospect of the cash rate rising from close to 0 per cent to around 1 per cent would inexplicably see the housing market 'crap its pants', for want of a better idiom.

That's my top-line take, regional variances notwithstanding.

Melbourne price growth is actually cooling, Perth has already flattened out, and Sydney's surge in listings is also calming things down a bit.

In Brisbane, though, as we have clearly seen on the ground, price growth has actually been accelerating, and Adelaide is also flying.

Of course prices will necessarily drop by a few per cent from their nominal peaks - whenever they prove to be - as they always will (almost by definition in a low inflation environment).

But nationally and in nominal terms, prices won't be falling any lower than today's levels, in my opinion.

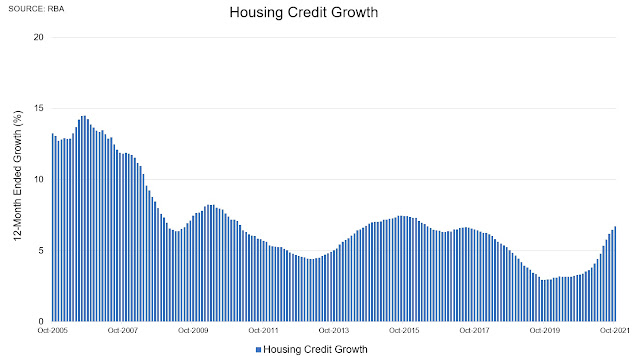

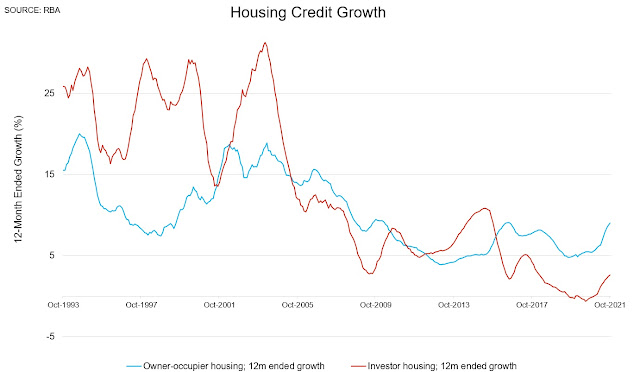

4 factors from housing market models

That's my take, anyway.

But what do the Reserve Bank discussion paper modellers themselves say about the prospects of a 30 per cent crash due to rising interest rates?

Well, clearly not, notes Trent Saunders, co-author of a key paper modelling Australian housing prices.

Here are four reasons why.

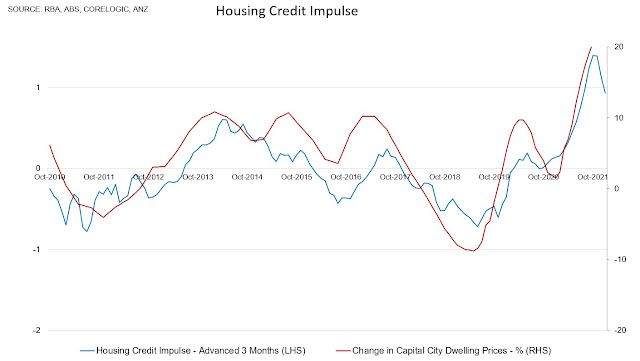

Firstly, because inflation is exogenous in the research discussion paper model, so modelling estimates are based upon changes in real rates.

Were inflation expectations were to move materially higher, therefore, then any related impact on housing prices would correspondingly be lessened.

Given the model was used in 2019 to isolate the impact of lower real rates, it doesn't make sense to translate estimates across to forecasts today, given that the context is not the same.

Secondly, the response of prices in the housing market model is non-linear, notes Saunders; so logically interest rate cuts should've had a greater impact as rates approached zero.

Thirdly, any impact on housing prices would be relative to baseline forecasts.

Thus, if forecasts were for housing prices to increase by, say, 2 per cent per annum, then only relative to these forecasts would the impact on prices be seen.

Fourthly, and moreover, as we

discussed in a recent article, such dramatic predictions or a crunch would need to assume no other change in macro variables, which is clearly unrealistic.

Improving economic conditions

In reality, in my opinion, we should be expecting employment growth and population growth to come roaring back over the next couple of years, comfortably offsetting even a potential 1 per cent increase in interest rates.

We also might expect hikes to the cash rate to be delivered in a considered and gradual manner, even if funding costs are rising.

We discussed some of these variables such as employment growth, the immigration reboot, fierce competition between lenders, low out-of-pocket expenses, and the ability of households to absorb higher repayments comfortably in this recent article

here (or click on the image below):