Data dump

Lots of data out today, which we'll parse here in a succinct manner.

Housing credit growth decelerated to 0.47 per cent in September, which roughly equalled the slowest pace of growth since November last year, according to the Reserve Bank's Financial Aggregates figures.

Year-on-year the pace of housing credit growth continued to slow to 7.3 per cent.

Having previously rebounded, property investor credit is now also being curtailed by stringent lending conditions and reduced borrowing capacity, increasing by just 0.32 per cent in September for the slowest month of growth since May 2021.

This reversal likely points to tight rental markets over the next couple of years.

Interestingly, although credit growth is decelerating for housing, for now the housing credit impulse doesn't appear to imply further any price declines from the current levels.

It was another very solid month for business credit, but broad money growth slowed from 0.2 per cent in August to 0.1 per cent in September.

Overall, housing credit is still likely to slow further due to reduced borrowing capacity, and very tough lending assessment restrictions.

Housing prices well off the highs

Further to the above, housing prices at the 5-capital city level are now -6.7 per cent below their high watermark, driven mainly by detached house prices in Sydney initially - especially at the more expensive end of the market - and more recently house prices Brisbane.

In saying that, the pace of decline at the capital city level has moderated in recent weeks.

In regional Queensland, we've seen some brutal repricing lower (for e.g. hinterland escapes, and for some coastal property), with expectations of the high sales prices from last year dashed by the more pessimistic outlook.

The AFR reported similar tales from the Mornington Peninsula down in Victoria.

---

Different this time?

The housing credit impulse indicator has been a pretty good predictor of housing prices over the past 15 years.

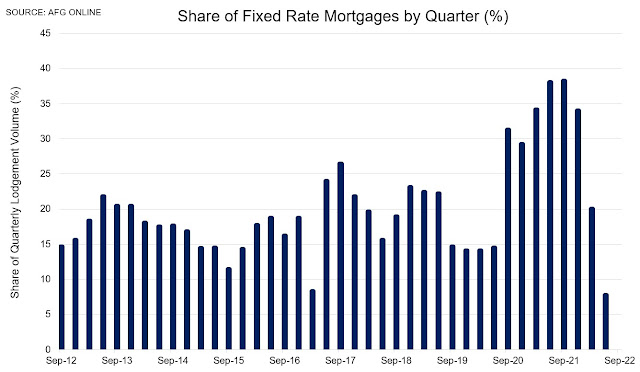

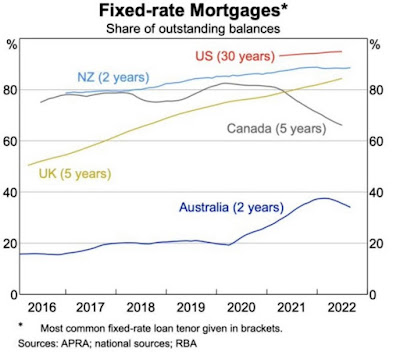

But this time 'may be different', in part because there's an enormous fixed rate mortgage cliff looming.

Normally fixed rate mortgages only account for a small share of the flow of housing lending in Australia.

But during the pandemic there were six consecutive quarters of extraordinarily high levels of fixed rate lending (from the September 2020 quarter through to the quarter ended December 2021).

Since the most common tenor of fixed rate mortgages in Australia is two years, this means that mortgages are just beginning to reset in earnest right now.

While we still have full employment and incomes are now rising - at least in nominal terms - a fixed rate mortgage resetting from 2 per cent to 6 per cent is bound to hurt.

Meanwhile many borrowers are trapped in a "mortgage prison" and unable to refinance due to the extraordinary 300 basis points lending assessment buffer, which has been built into lending serviceability expectations since October 2021.

---

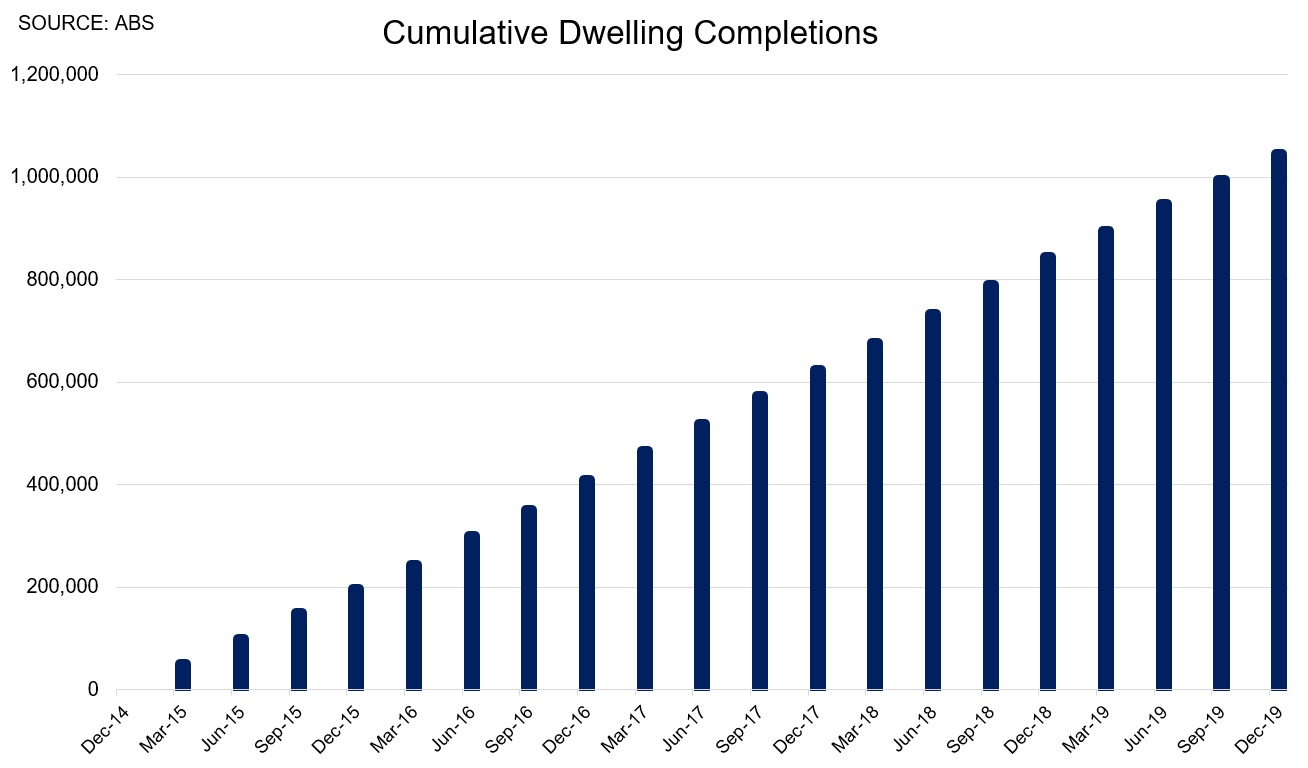

The dwelling stock increased by only 1.4 per cent over the financial year to June 2022, which was the slowest rate of increase in many a year.

Source: ABS

While there were approximately 174,100 additions to the Aussie dwelling stock, there were also more than 27,200 demolitions and removals.

This took the total number of dwellings to 10.9 million.

Still, some of the rapid rates of housing construction in the distant outer suburbs of the larger capital cities are leading to chronic traffic congestion in those areas.

As as 30 June 2022 there were a record number of dwellings still under construction, with some projects delayed due to the price or availability of materials, so we should still see a strong number of detached housing completions over the coming few months.

Household goods retail cooling

Retail turnover was less convincing in September, rising by 0.6 per cent, with a mini-boost for food retailing and outlets.

There was a national day of mourning and an extra public holiday in the month, somewhat boosting expenditure on eating out.

But the monthly result was overwhelmingly accounted for by stronger prices rather than rising retail volumes, and sales of household goods barely budged in the September quarter.

Year-on-year growth retail turnover is now in decline, and this is set to continue over the next 18 months as rising interest rates since May, falling real wages, and the fixed rate mortgage cliff begin to bite.

The monthly inflation gauge from the Melbourne Institute also slowed to 0.4 per cent from 0.5 per cent last month.

The trimmed mean reading increased by only 0.3 per cent in September, presumably locking in tomorrow's interest rate decision at a more sedate 25 basis points.