Jobs growth muted

With jobless claims remaining at around 50-year lows there's been no 'smoking gun' showing a dramatic slowing in the US economy, and the ADP employed figures this week were also solid.

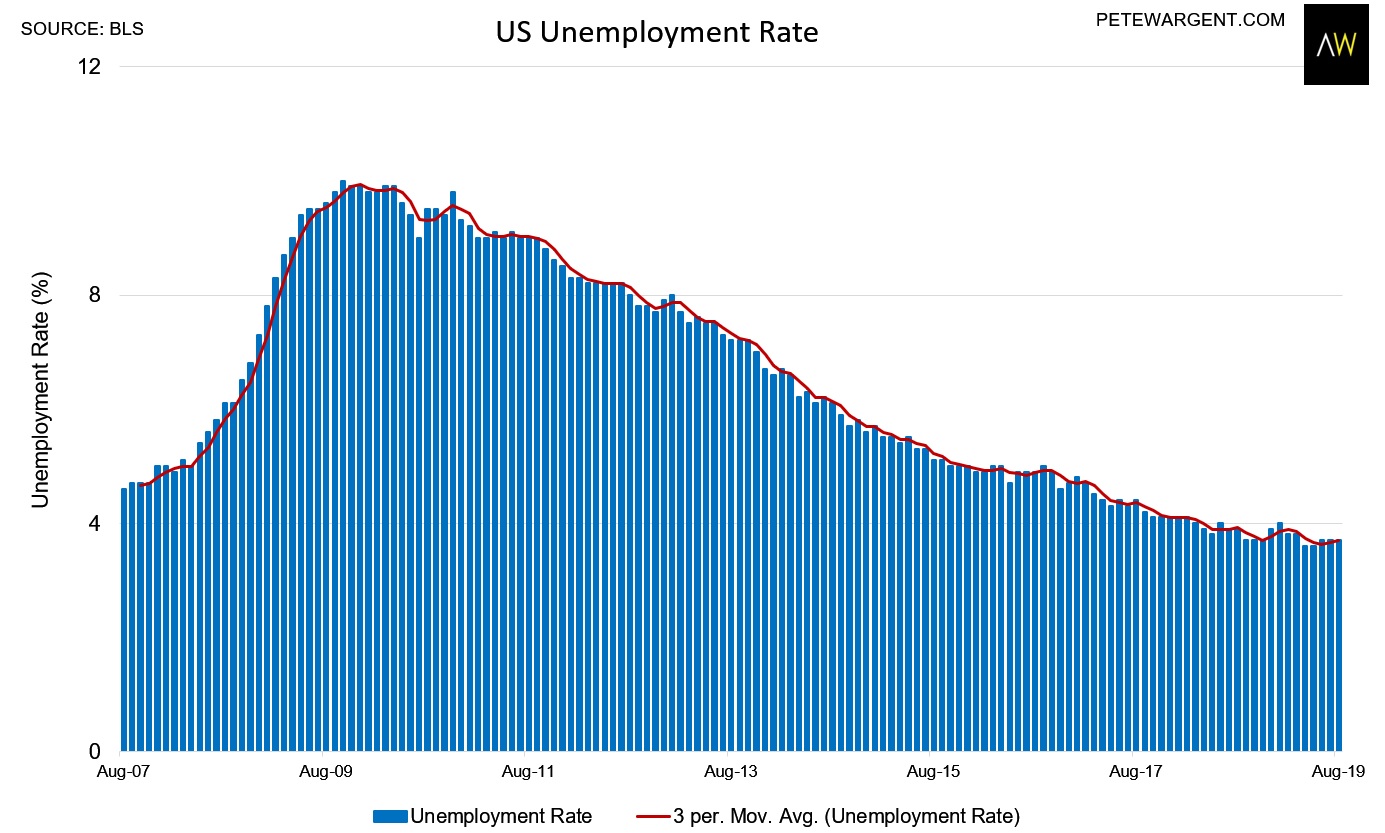

All eyes turned to the Bureau of Labor Statistics figures for August 2019, and there was a bit of something here for everyone.

Employment increased by a record 107th consecutive month, but only by +130,000 this month (well below market expectations of +150,000), while a fair chunk of the increase related to temporary government employment for the Census count.

Accordingly private sector jobs growth was estimated to be under +100,000 for the month, while there were combined downards revisions of -20,000 to the two preceding months.

Still, though, you can hardly argue that the 3-month average employment growth of +156,000 is too bad at this stage of the cycle!

The employment to population rate increased to an expansion high of 60.9 per cent, the highest level since 2008.

And the unemployment rate remained very low at just 3.7 per cent, albeit just a notch about the half-century lows.

There was still no sign of rapidly rising earnings, with average hourly pay up still by about 3¼ per cent year-on-year, about 1 per cent ahead of inflation.

Not often mentioned, earnings have been outpacing inflation in the US for nearly 7 years now.

Further easing?

US 30-year mortgage rates are now below 3½ per cent, to be at the lowest level since 2016, while other central banks from Russia to China are busily cutting or easing policy.

Inflation expectations in the US have also dropped to about 1½ per cent, to be at the lowest level since 2016, so there is room for the Fed to cut rates if required.

However, markets are only pricing about a 1 in 4 chance of a cut in a fortnight's time, with today's release deemed to be reasonable enough.

Overall, there wasn't really too much in these figures to be getting bearish about.