Inventories drag

The Q4 business indicators for the Aussie economy came in a bit soft, overall.

Mining profits had an absolute bonanza through 2021 and 2022, and it looks as though the quarterly peak in profits fell in the June quarter of 2022.

Previously strong quarterly mineral exploration is now set to follow commodity prices lower, with a modest quarterly decline in expenditure to around $1 billion led down by gold exploration spend.

The total wages and salaries bill in Q4 increased by +2.4 per cent, rounding off a strong rebound in activity for 2022, although it looks as though the strongest part of the rebound was also experienced around June 2022.

The quarterly sales figures came in very soft, however, all but stalling in the final quarter of the year.

Domestic demand appears likely to be barely positive in Q4, and inventories will be a significant drag on growth in the final quarter of 2022, subtracting a significant -0.8 percentage points.

There are more figures to come in yet, but evidently economic growth in Q4 is going to be soft, and possibly negative in per capita terms.

Rental crisis accelerates

APRA announced yesterday that the 300 basis points lending assessment buffer will remain in place for the time being, presumably until there is greater certainty around where the terminal cash rate for this cycle will be.

The dilemma is clear enough - having missed the inflation target on the low side for half a decade, policymakers and regulators can't afford to appear similarly half-arsed about bringing inflation back down to the 2-3 per cent range.

Thus we may expect the tough talk to continue for a while yet.

The cost of this will be a continuation of the rental crisis in some parts of the country.

In the short-term there may be some respite as the long pipeline of completions comes onto the market, however...

Unit supply set to shrink

Over the next two years, Charter Keck Cramer's latest report anticipates a -73 per cent decline in unit supply, led by a decline of -84 per cent in Sydney, and -65 per cent in Melbourne.

Sydney's unit commencements have slowed continuously from 31,000 in 2017 to just 7,700 over the latest financial year,

reported the AFR, just as population growth ramps up.

Brisbane unit commencements have similarly dropped from 13,300 in FY2016 to just 1,900 in FY 2022.

Charter Keck Cramer reported that unit prices would have to increase within months due to the chronic shortage, and indeed they already are in Brisbane.

The Housing Industry Association (HIA) has also warned of "long and dangerous lags" associated with ongoing interest rate increases.

I was chatting to a guy this week who is currently living in a parking space (Sunshine Coast), but that said it looks as though the main rental pressures this year could well be felt in Sydney and Melbourne as immigration restarts fully.

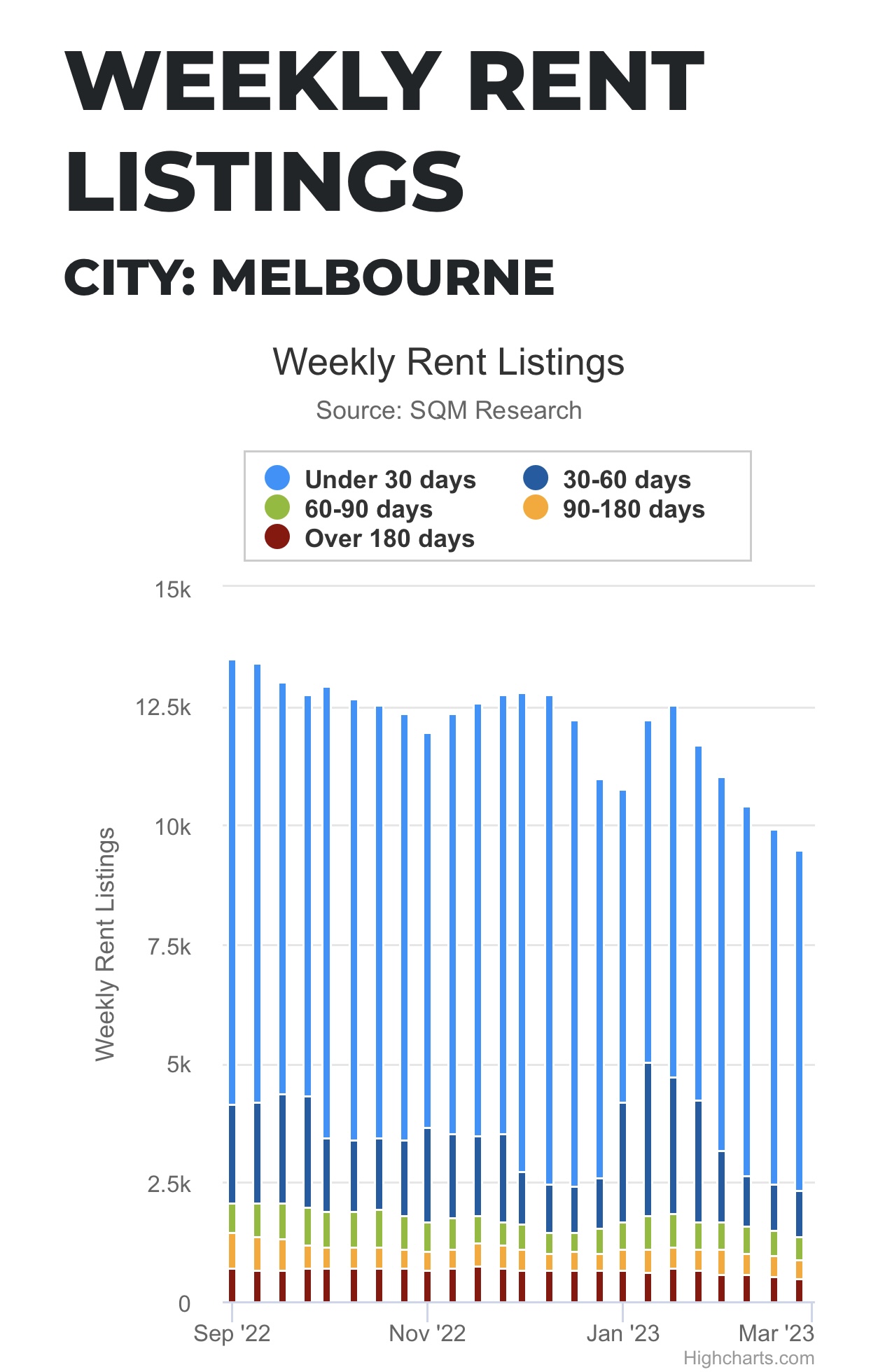

In Melbourne, total rental listings hit another all-time low this week, according to SQM Research, with population growth now set to accelerate.

Source: SQM Research

Asking rents for units in Melbourne (and Sydney) are now almost going vertical, rising +7.4 per cent over the past quarter.

Source: SQM Research

Looking further ahead, Australia is set to embrace the eco-socialist utopia of "Build to Rent" tower blocks, especially in Melbourne, from around 2026, so renters can "own nothing and be happy" (with the UK leading the idiotic charge for limiting social movement to a 15-miute radius from your home. Something else to be resisted at all costs!).

More hikes to come

Despite the above challenges, economists have been calling for more rate hikes, goaded along by market pricing in the US, although pricing in more hawkish policy at this late stage in the cycle arguably encourages the market to price in more and faster interest rates cuts when they do arrive.

Source: ANZ, Bloomberg

---

Unfortunately as the rental crisis and homelessness increases, that means we're consigned to another month of debate on the Noosa Community Notice Board of whether Victorians should be banned from leaving the state.

Borderline unhinged, I know, but rental markets are becoming extremely tight right now, and lending assessment settings are now set to be tightened even further.