Old news, of course, but S&P Global released their latest mortgage arrears data for Australia.

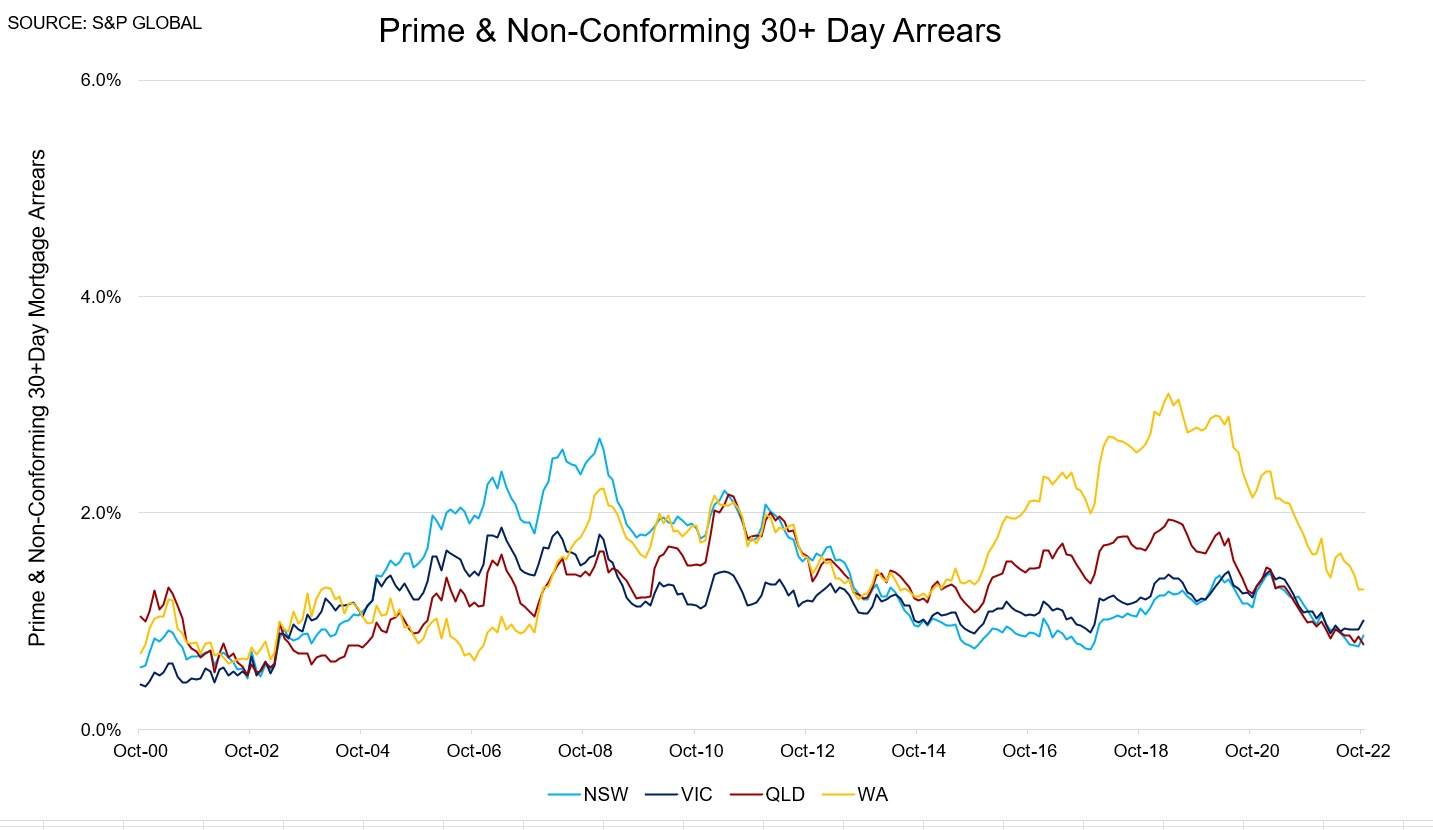

Prime 30 plus day mortgage arrears were extremely low at 0.69 per cent.

This isn't too surprising given full employment, record low vacancy rates, and surging rents.

The question is how much they will rise by in 2023 as rising mortgage rates begin to hurt borrowers.

We may just be seeing the first signs of an increase as rising mortgage rates start to bite, but from record low levels.

A key difference from previous cycles is that whereby 100 per cent mortgages and low-doc loans were once commonplace, today they're no longer a key feature of the financial system.

Non-conforming arrears ran to an alarming 23 per cent in the early 2000s downturn, but tighter lending standards have made a world of difference to systemic risks since the global financial crisis.

Variously Western Australia (mining downturn) and Queensland (flooding) have had elevated mortgage arrears over the past decade, but this is not the case at present.

Recent history suggests that the most highly-leveraged Sydney households could face the bulk of the stress from rising mortgage rates in 2023.

However, mortgage lending standards are a world apart from the pre-GFC days, and the impact is most likely to be seen in declining household consumption, such as for household goods and recreation expenditure.