Great to be back on the BIP Show talking office assets, residential property news, and more.

Tune in here (or click on the image below):

Episode 1

Tune in to the Australian Property Podcast on Apple podcasts, Spotify, or at the main website.

Or, you can simply watch on YouTube here:

European pressures

With the UBS/Credit Suisse takeover dominating news flows over recent days, jittery financial markets turned their attention towards fellow struggler Deutsche Bank.

Deutsche's share price is down -26 per cent to EUR 8.50over the past month as fears of a default rise (and is of course way down from pre-financial crisis highs of around EUR 92).

There are the usual charts showing an alarming spike in credit default swaps over recent days.

Zooming out the graph to a decade timeframe is still pretty alarming, but at least shows the situation in some broader context.

Source: Bloomberg Terminal

Germany Chancellor Olaf Scholz moved quickly to announce that the banking system in Europe is stable, which naturally brought to mind the old Thatcher adage that if you need to state that you're powerful then you probably aren't (or something like that).

Whatever, global markets have been further shaken to the extent that futures have priced interest rate cuts in the US beginning as soon as June.

Not sure about that but in any event the trend will inevitably be down over the next few years.

---

Domestic news: tent cities

There are two keys news items this week in Australia.

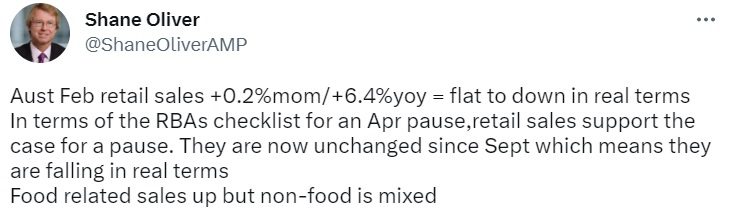

Firstly, retail turnover, which is expected to be flat in nominal terms for the month of February, with domestic demand now fading.

And then there's the monthly inflation release, which is volatile and incomplete, but nevertheless watched by the Reserve Bank for an indication of whether a pause in interest rates is now appropriate.

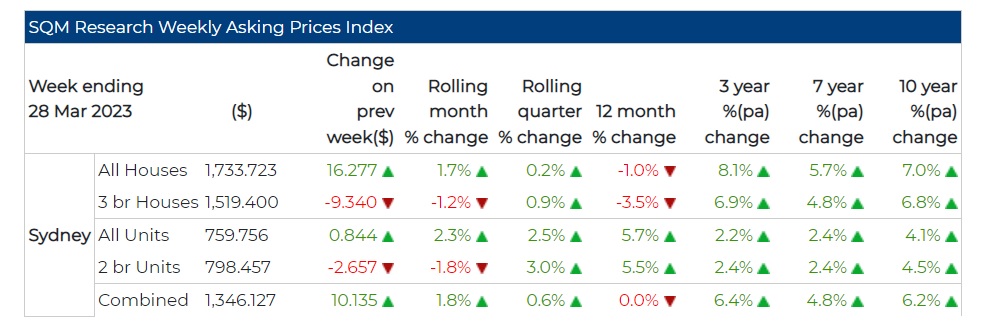

Housing markets have continued to firm over the past 8 weeks in the face of a looming chronic shortage of rentals in the capital cities, with steady selling price increases also set to be reported.

Most weeks now there are reports of tent cities popping up in Australia.

Last year they were mainly being pitched in regional areas, but now they're popping up in the capitals.

Properties coming up for rent in Sydney and consistently seeing rents being repriced 30 to 50 per cent higher due to the ongoing dearth of new landlords in the market and skyrocketing demand.

Labor won the NSW election at a canter yesterday, having campaigned hard for tenant rights, including ending unfair evictions by landlords.

We'll have to see how that plays out, though it's unlikely to encourage more rental stock (well, actually the opposite).

The settings are all wrong for the city rentals market at the moment: record high immigration, workers moving back into town from regional Australia, higher interest rates being quoted for investor borrowers, and a nanny state lending assessment buffer accounting for a hypothetical 12 interest rate hikes scenario (when futures markets are expecting rate cuts ahead).

A 50 per cent step-up in Sydney rents is pretty much locked in while those settings remain in place.

Inflation easing

The US Federal Reserve lifted the Funds Rate by 25 basis points overnight - very likely the final interest rate hike for this cycle - sending the bank indices into a bit of a tizz.

Powell's speech revealed a dovish tilt, however, and interestingly financial markets are pricing for 3 or 4 interest rate cuts ahead by January next year.

Bond yields also dropped back in Australia on the dovish rhetoric.

The most US recent data released yesterday suggests that inflation pressures are still easing overall.

The dynamic in Australia is somewhat different.

In contrast to the US, wage price growth Down Under is only running at a very modest 3.3 per cent, and now appears to have peaked as immigration ramps back up.

And with most borrowers on variable mortgage rates - or short-term fixed rates - spending is already slowing sharply.

ANZ observed services spending in March as being down by more than 12 per cent from a year earlier, with softness in evidence across the board.

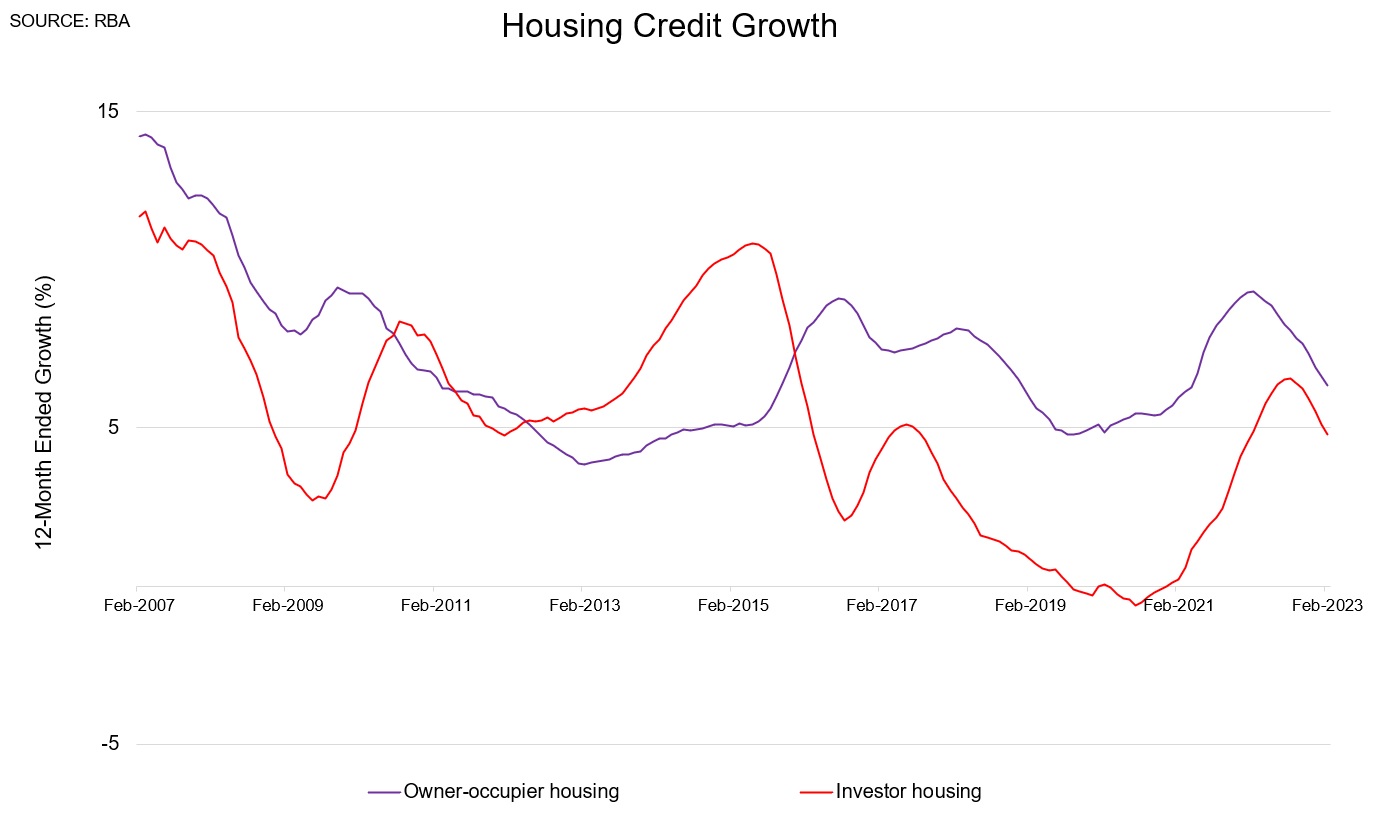

A critical emerging issue in Australia is the enormous build-up of pressure in rental markets, especially in Sydney, with rapid immigration returning and a tight regulatory squeeze being maintained on investor borrowers.

Mortgage rates are generally higher for investors, and stress-testing is being carried out at extremely tight level - with no apparent justification, especially now given record low rental vacancies and the skyrocketing trajectory of rents.

Source: SQM Research

It's hard to see how this can be sustained, so something has to give.

Supply shocks solved

Charlie Bilello always provides sensational insights from the US on Twitter, and is well worth a follow.

From this weekend alone...freight costs are now - almost unbelievably - lower than they were at the start of the pandemic, having plummeted by an astonishing -87 per cent.

On the rampant demand side, things have been gradually cooling a bit too.

The average price of a used Tesla has fallen by US$21,000 since July last year, as charted by Charlie:

Gas prices are now tracking -20 per cent lower than a year ago.

In Australia we aren't quite there yet, but given the significant drop in oil prices of late it shouldn't be too long before unleaded prices are down by a similar amount from a year earlier (diesel prices have remained strangely high, on the other hand).

As for US interest rates? Well, they are now expected to fall now over the next two years, as markets price in rising concerns about major stress within the banking system.