Interstate wave

South-east Queensland is now by far the most popular destination for Aussies, and population growth in the state has surged ahead.

I took a quick look at the stats here (or click on the image below):

UK immigration surge

The UK Daily Telegraph reports that more than 1 million foreign nationals were allowed to live in the UK in a single year, an increase of 35 per cent, breaking one of the key Brexit pledges to regain control of the borders.

---

Following the controversial Brexit vote, the UK has seen more than 1 million foreign nationals to live in the country in a year.

Of course, visas granted to EU citizens increased as expected.

But the real shock to Brexiteers has been the huge surge in non-EU visa grants, study grants, illegal arrivals, and other non-EU categories.

Migration Watch charts the latest non-EU ONS figures below:

Source: Migration Watch

There is likely to a battle for the best and brightest international students between countries like Canada, the US, the UK, and Australia...and the UK is off and running with 411,800 study grants to non-EU nationals, hugely outstripping the record 285,500 seen in 2019.

The outdated National Health Service is already buckling after years of under-funding and failed attempts to modernise, so this will add to the pressures.

Meanwhile, inflation in the UK is heading towards 10 per cent as energy and power prices surge.

---

I looked at how Australia's population growth is likely to rebound here.

The competition for international students is likely to be a key plank of migration policy over the next few years.

Construction outlook

Engineering construction has been fairly flat over the past couple of years, even in Western Australia and the coalfields, despite extremely high commodity prices.

The Reserve Bank is confident that construction will remain solid for the next two years.

These figures cast some doubt on that view.

In truth, there were factors which probably pulled down the March result - some related to COVID shutdowns, and some related to the fortnight of flooding in Queensland and New South Wales - and the June figures will probably record a bounce as the rain eased.

Another possible factor or explanation is that capacity constraints, the high cost of building materials and trades services, and numerous current and potentially looming insolvencies in the sector are starting to drag the cycle lower in line with falling building approvals.

Maybe it was a bit of both.

---

The Reserve Bank's Luci Ellis delivered another excellent speech on housing market trends through the pandemic, and the outlook.

It was interesting to see estimates on the decline in the average household size, the COVID impact on inner-city housing prices, and the expected rebound in population growth.

Well worth a read, as always.

Property Pod

This week on the podcast, the legendary Owen Rask joins me to talk investing in stocks, property, and super.

Owen discusses his family background, escaping from Europe, his challenging upbringing, and how he turned his passion into a business.

Tune in here (or click on the image below):

.png)

You can also tune in at Apple podcasts, Spotify, or wherever else you get your podcast fix.

And you can tune in at Youtube here:

Rental crisis easing a touch?

Rental vacancies were stone dead flat in Sydney in April, at 12,758, according to SQM Research's latest figures.

Melbourne recorded a modest rise from 12,400 to 12,655 vacancies, though this still meant a flat result in percentage terms for the Victorian capital at 1.9 per cent.

This was driven by a jump in rental vacancies in the CBD, where the vacancy rate gapped a bit higher from 2.4 per cent to 2.9 per cent.

Brisbane also recorded a flat result at a 0.7 per cent vacancy rate.

The trend in the major capital cities may still be down, despite flat results for the month.

All other capital cities, which have seen extremely tight rental markets in recent months, recorded an increase in vacancy rates in April.

This is the first time we've seen an increase in rental vacancies in 2022, with the national residential rental vacancy rate increasing slightly from 1 per cent to 1.1 per cent, according to SQM Research.

Certainly in my neck of the woods (Noosa) there has been some tenant pushback against surging rents, and some properties are lying empty as a result.

Asking rents have increased 20 per cent year-on-year for housing in Sydney, Brisbane, and Adelaide, and 10 to 15 per cent elsewhere, according to SQM's asking rents index.

It's worth noting that not all markets have seen such strong increases, and there may be something of a base effect in these numbers (i.e. in many cases rents went down, and now are going back up again).

Source: SQM Research

Overall, there may be some easing of the rental crisis underway, but it hasn't stopped landlords raising asking rents by another 1.4 per cent over the past 30 days, according to SQM Research.

---

The RBA released its May Meeting Board Minutes this morning.

It appears that if the wage price index figures are strong tomorrow the cash rate target could well be lifted by 40 basis points in June, to 0.75 per cent...but let's see.

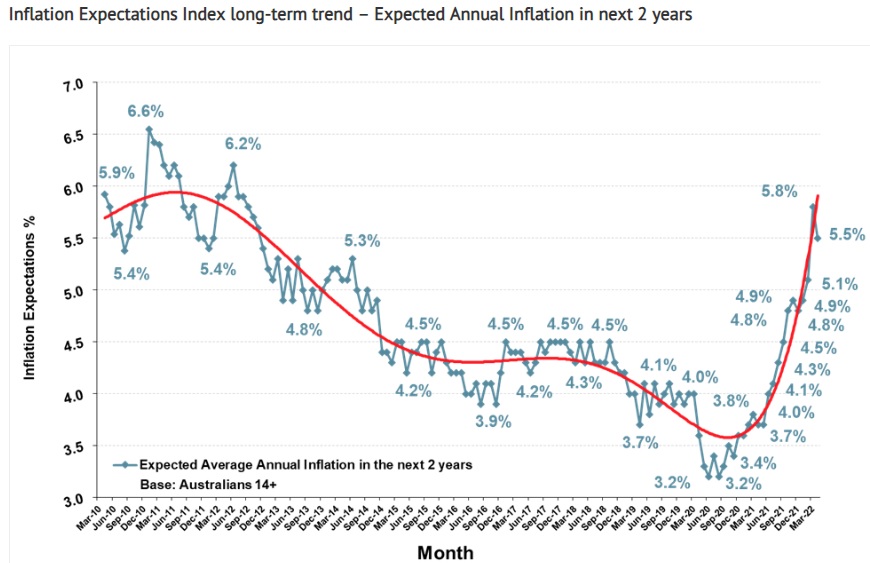

Inflation peaking

The TD-MI monthly inflation gauge turned slightly negative on the headline measure last month, at -0.1 per cent in April.

Now Roy Morgan sees inflation expectations ticking back down from 5.8 per cent to 5.5 per cent, for the same month.

Source: Roy Morgan

The main driver was the fuel excise cut, and brings inflation expectations back into line with where they were from 2009 to 2014 (when the actual underlying inflation rate was in the target band).

.png)