Inflation pressures by 2023

There's been some very excitable talk about the recent moves in bond yields.

For some reason the prospect of higher interest rates always generates an adrenaline rush of social media excitement...even though the trend in interest rates has been down for several decades.

Some fixed rate mortgage products have been nudged 10 basis points higher this week.

And it's true that yields have been rising, while the target bond yields have not been so easy to come by lately...

The April 2024 bond eventually traded down at 0.125 per cent after the close, but evidently the pressures are there.

Board Minutes

Some pausing for alternative thoughts, though.

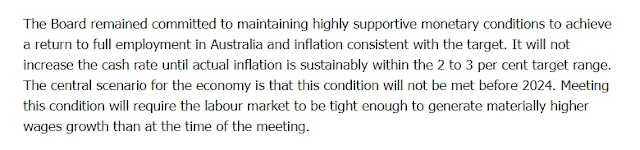

The Reserve Bank of Australia released its latest Board Minutes today, and they suggested very little change to the proposed policy approach.

The RBA still wants to see inflation sustainably back in the 2 to 3 per cent target band, but noted that to date there are few indications that wages growth is set to lift meaningfully or accelerate sharply in Australia over the period ahead.

For this reason, no interest rate moves are to be expected before 2024, according to the latest Minutes.

Source: RBA

Furthermore, no case is seen for less accommodative policy to slow housing prices or credit growth.

The lack of punch from wages growth is before the international borders are reopened, fuelling the return of tens of thousands of international students, new migrants, and other temporary visa holders.

All of which could presumably depress the prospects for wages growth again.

For these reasons the bank will continue to target bond yields for the time being.

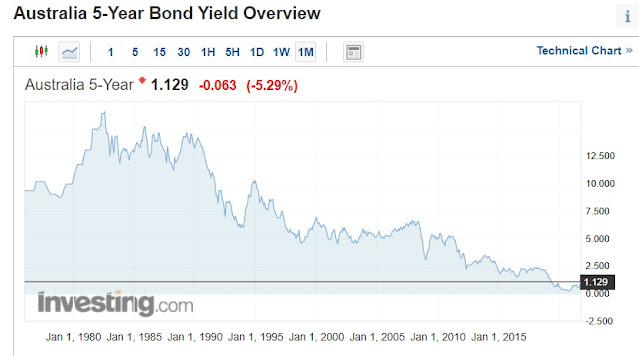

Finally for some perspective, and looking further out, the 4-year bond yield is still trading under 1 per cent, and although the 5-year yield is off the lows, it's not exactly sky-high at 1.129 per cent.

Overall, an interesting dynamic is forming, with competing forces pulling in different directions.