Rental shortage ahead

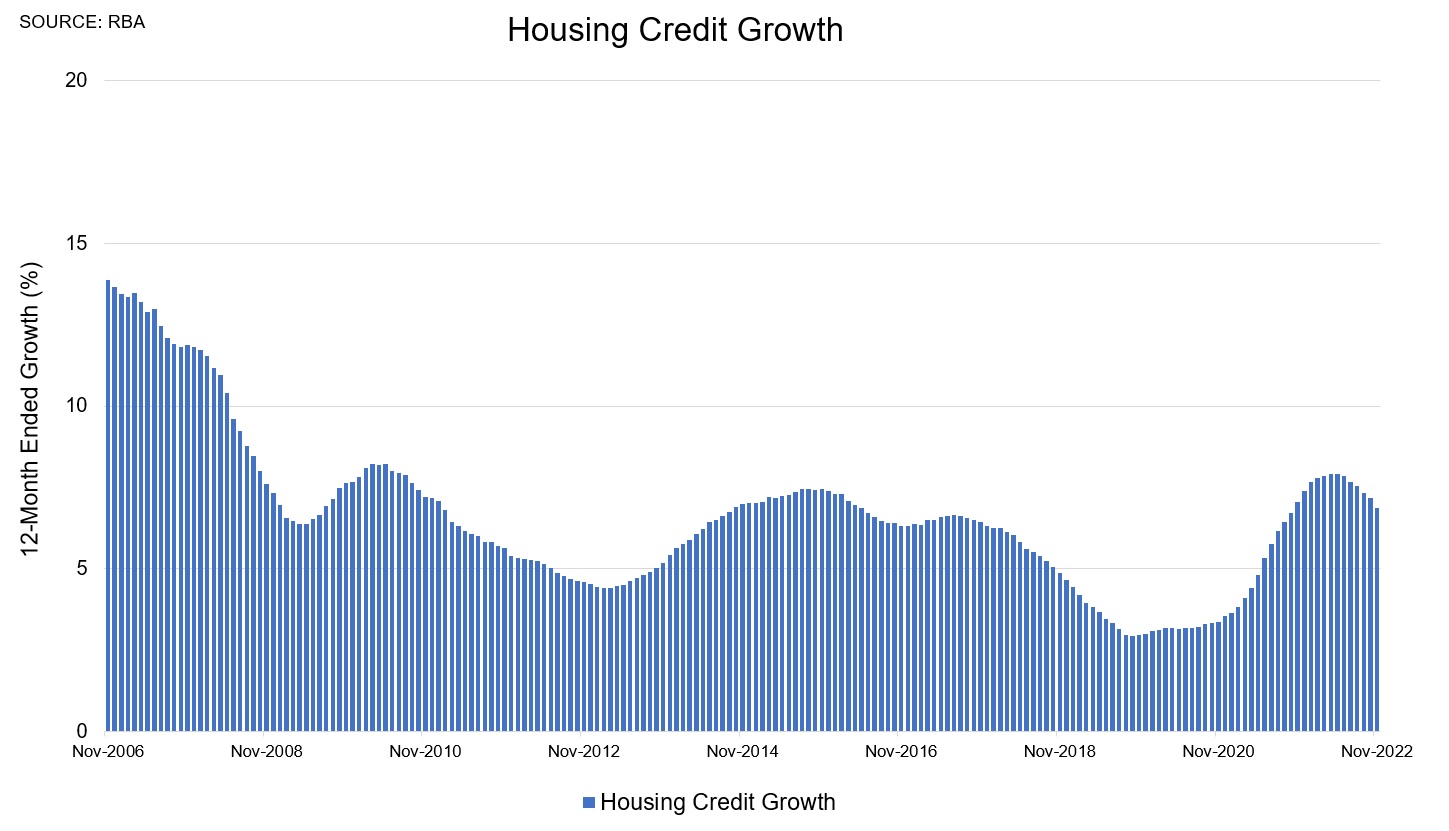

Credit growth was revised down to 0.54 per cent for October, and the November figure was just 0.49 per cent.

Annual credit growth thus dropped sharply from 9.3 per cent to 8.9 per cent in October, and we can expect the annual figure to drop much further from here.

Housing credit growth has slowed to 0.4 per cent over the past couple of months, and the 3 month annualised pace is now way down from the highs at around 5 per cent.

The main driver of this has been investor credit, which over the past two months has slowed to a crawl, at under 0.3 per cent.

Even if investors wanted to come back into the market to address the chronic shortage of rentals, many are unable to do so due to the restrictive lending assessment buffer at 300 basis points.

The housing credit impulse took a leg lower after the revisions to last month's figures, with capital city prices now about 8½ per cent below their highs.

Property investors tend to become despondent at this stage in the cycle, with borrowing capacity still severely curtailed for many borrowers, even in spite of rocketing rents and rising household incomes.

On the other hand, I can't ever remember a time when we were headed for such a chronic shortage of rental properties, with many instances of rents rising by 25 to 30 per cent over the past year in Sydney and other capital cities.

Immigration is set to rise to unprecedented highs next year.

For reference the UK has already seen net immigration explode to an all-time highs as visa backlogs are cleared, while Canada's population growth has hit an all-time high of +865,000 over the year.

Of course, Australia is next cab off the rank as the huge visa backlog is cleared, and this at a time when new home sales have crashed back to their pandemic lows.