CapEx also falling

Oh dear.

The manufacturing index slumping to a deeply contractionary reading of 44.7 was immediately followed by a negative result for CapEx.

Private new capital expenditure slumped by -0.6 per cent in Q3, well behind market expectations.

Notably equipment spend, which was expected to rebound handsomely, fell by -1.9 per cent.

This has implications for real GDP, which seems increasingly likely be poor as consumption volumes shrink.

The underlying details of the report were weak, according to the great analyst James Foster, who noted that the only supporting factor for investment was non-mining construction.

While private new capital expenditure was up by 9 per cent over the year in New South Wales, Western Australia saw investment shrink by -5 per cent.

At the sector level. retail investment was weak as the consumption outlook sours.

Investment plans for 2022/3 were broadly as expected at around $155 billion, but overall this was another a string of weaker than expected reports on the state of the economy.

It's worth noting that these figures relate to the period before the interest rate hikes in October and November, so the outlook is only likely to soften from here.

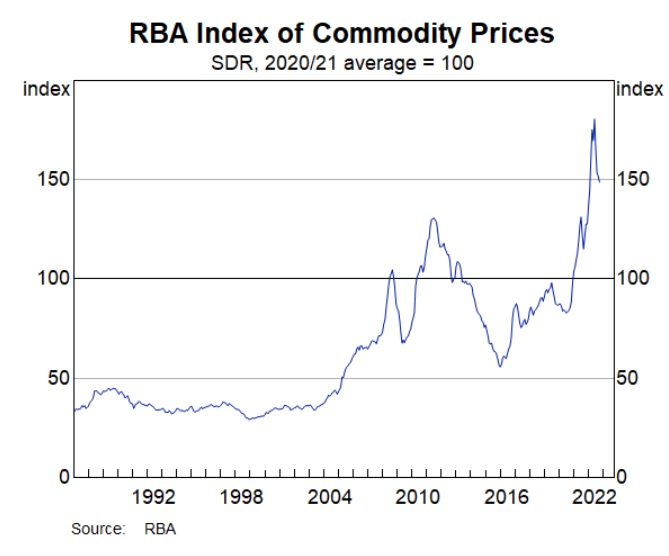

High commodity prices

With inflation already having peaked according to the monthly inflation figures, there's little need for monetary policy to be tightened further.

Australia is likely to face headwinds enough as the commodity price index mean reverts from all-time high reading towards the long-run average.

Sky-high commodity prices possibly in part account for why Australia's stock market index isn't too far below its recent highs.

Commonwealth Bank's Gareth Aird sees one more interest rate hike to a terminal cash rate target of 3.10 per cent, but some other analysts are calling for several more hikes.

---

Back to the city

Louis Christopher of SQM Research and Catherine Cashmore of Cashmore & Co. property discussed on a recent podcast the demographics of the return to the city, and the rising risks for illiquid housing markets.

Source: SQM Research