Inflation decline

I had a suspicion the monthly inflation figures were going to be down year-on-year, based on the partials available.

As it turned out, even that optimistic expectation was well overcooked, with monthly inflation coming in flat for a massive drop in the year-on-year reading, all the way back down to 6.9 per cent (against a market expectation of 7.3 per cent).

Note that some market forecasters were looking for 8.3 per cent, so it was a big beat.

The building approvals figures also came in at the bottom end of the market forecast range, dropping another =6 per cent in October, taking annual building approvals down to a 21-month low of 192,660.

Inflation has largely (though not totally) been driven by supply-side factors such as global supply chain disruptions, the international border closures and related labour shortages, the Ukraine war, and repeated bursts of flooding in Australia.

The good news is that the reopening inflation "belch" now appears to be passing.

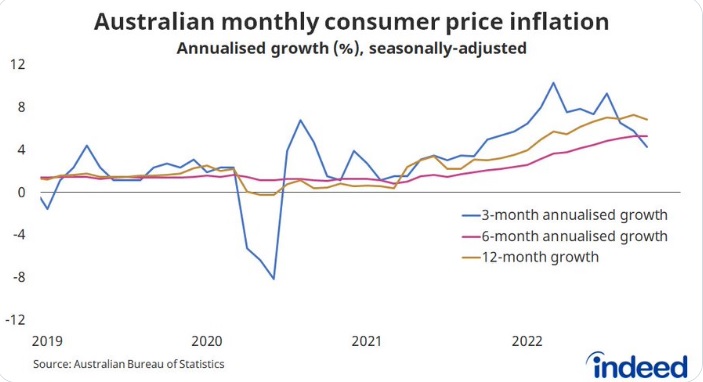

Callam Pickering, Chief Economist of Indeed, shows how the inflationary pulse is now falling away over the past few months.

In the event the Aussie dollar rebounded from 62 US cents back up to 67 US cents (and in any case its the trade-weighted index measure that should hold more sway from a currency perspective).

There was the usual questioning about whether the inflation figures were 'right' or not, but financial markets clearly saw today's data as meaningful.

Australia's 3-year bond yield has declined from 3.8 per cent in September to 3.16 per cent today.