Book launch from an old buddy of mine, Dave Gow.

You can order a copy here (or click on the image below):

Get around it!

The bezzle

In the 1950s economist John

Galbraith coined the concept of the ‘bezzle’, defined as the inventory of

undiscovered embezzlements in the economy.

The bezzle increases during periods of irrational exuberance in the markets and before the victims become aware of the fraud.

In good times, funds are plentiful and investors too

trusting, but in recessionary times these dynamics are reversed.

The creation of the undisclosed bezzle can be doubly powerful in stimulating spending in the economy as wealth and leverage increases.

But ultimately the reversal and destruction of

fictional wealth will have an equivalently strong impact via the negative

wealth effect.

Recent periods of zero interest rates unleashed speculative excesses on an epic scale, but much of the perceived increase in wealth is proving to be illusory.

As central bankers dial

interest rates back up from the zero lower bound, consumers are becoming

increasingly alert to the shrinking of the bezzle.

The waves of government stimulus

rolled out through the pandemic may have been necessary but were also bound to

become another significant source of bezzle in the economy.

Illusory wealth

While the bezzle might be most

aptly characterised by the most infamous frauds, fugazzis, and Ponzi

schemes, such as the Bernie Madoff swindle, asset prices levitating far above

their fundamental or productive values can also create unsustainable or illusory

psychic wealth across equities and housing markets.

In the residential property

market space, Australia’s hinterland boltholes and coastal escapes which were

frequently selling sight unseen through the pandemic and attracting ebullient

$3 million bids have been repriced lower towards $2 million, and brutally so in

some cases.

The bulk of the $½ trillion unwind in Australian housing equity to date has largely stemmed from the upper price quartile.

This includes sectors of the market which benefited most from the zero

interest rate policy and the ‘race of space’ away from higher-density city

living and apartment towers with unusable shared facilities.

The bottom end of the residential housing market has to date held up in a more robust manner, which will be a welcome relief to the recent first homebuyers who took advantage of the government’s first home loan deposit scheme.

This partly

reflects the steep increase in building materials and trades costs, which has

underpinned the lower end of the market, as well as sharply rising rents.

New South Wales Premier

Perrotet has also successfully passed the historic first homebuyer law through

Parliament, which will reduce upfront costs for first homebuyers entering the

market in the state prospectively and is set to increase first homebuyer demand

up to the $1.5 million price point.

Overall, however, market

sentiment remains cautious for now, and will likely remain so for as long as the

cash rate target is being ratcheted higher.

Fixed rate pain

Historically, Australia only

had around one-fifth of mortgage balances on fixed rate products, but this

market share ballooned from the September 2020 quarter all the way through

until the end of 2021.

With the most common tenor of fixed

rate mortgage in Australia being two years, the fixed rate cliff is now kicking

into gear, and the ensuing reset will send a few tremors through household

balance sheets, in turn impacting the consumption of household goods and

services.

In the commercial real estate sector, secondary-grade office space which was previously selling on record low yields also faces challenges.

Rents are falling as weak tenant demand and low

office occupancy rates have persisted long after the most onerous of the COVID-19

restrictions passed, in turn shifting demand into the discounted A-grade stock.

Galbraith posited that the

bezzle is eliminated during periods of growing trepidation in the markets, with

much of the reversal in paper wealth typically being absorbed by retail punters

and ordinary households.

For now, each month tighter monetary

policy is sucking money out of the economy, and investors have become more sceptical.

We shouldn’t be too surprised.

As Galbraith foretold, every bezzle ends.

Impulse improves

Housing credit growth slowed in October, but less sharply, to 7.2 per cent.

The rate of change or 'credit impulse' seems to suggest that the worst of the housing price declines are now done with (but a lot depends on the outlook for interest rate changes, so let's see).

The rentals market looks to be in dire straits, not helped by extremely tight lending assessment criteria.

Anecdotally, landlords are increasingly looking to increase rents on lease renewals at 10 to 20 per cent higher than a year earlier.

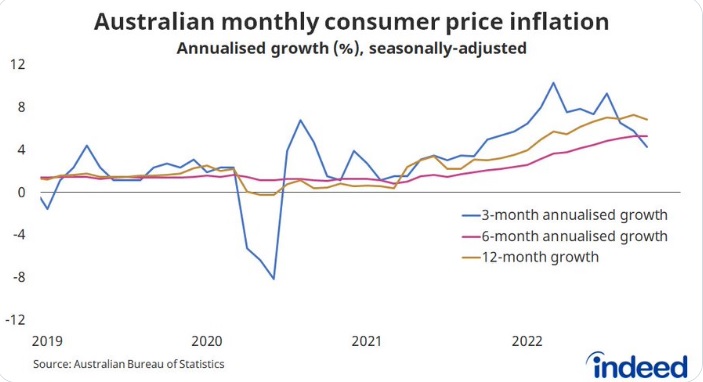

Inflation decline

I had a suspicion the monthly inflation figures were going to be down year-on-year, based on the partials available.

As it turned out, even that optimistic expectation was well overcooked, with monthly inflation coming in flat for a massive drop in the year-on-year reading, all the way back down to 6.9 per cent (against a market expectation of 7.3 per cent).

Note that some market forecasters were looking for 8.3 per cent, so it was a big beat.

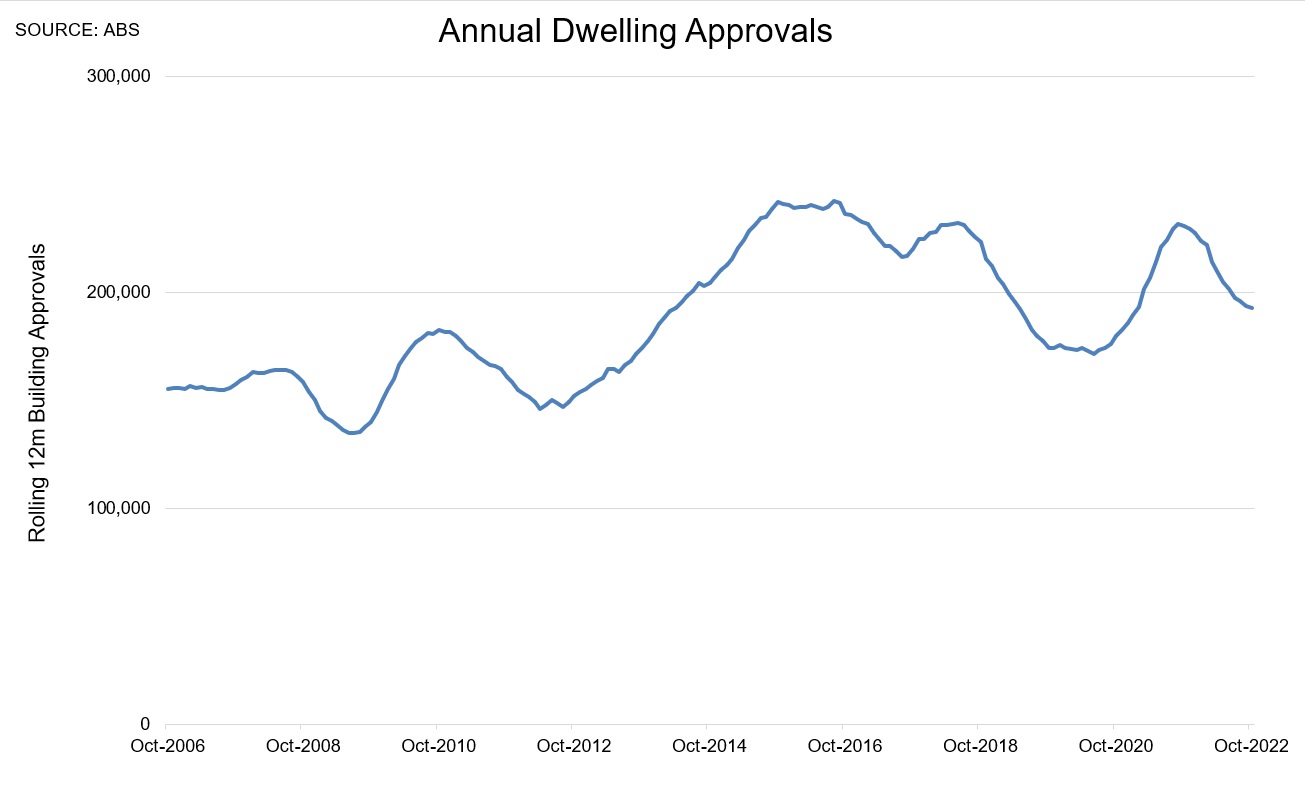

The building approvals figures also came in at the bottom end of the market forecast range, dropping another =6 per cent in October, taking annual building approvals down to a 21-month low of 192,660.

Inflation has largely (though not totally) been driven by supply-side factors such as global supply chain disruptions, the international border closures and related labour shortages, the Ukraine war, and repeated bursts of flooding in Australia.

The good news is that the reopening inflation "belch" now appears to be passing.

Callam Pickering, Chief Economist of Indeed, shows how the inflationary pulse is now falling away over the past few months.

In the event the Aussie dollar rebounded from 62 US cents back up to 67 US cents (and in any case its the trade-weighted index measure that should hold more sway from a currency perspective).

There was the usual questioning about whether the inflation figures were 'right' or not, but financial markets clearly saw today's data as meaningful.

Australia's 3-year bond yield has declined from 3.8 per cent in September to 3.16 per cent today.

Visas rocket back

.png)

Rental supply shrinking

The Reserve Bank Governor spoke before the Senate Economics Committee today, and noted that Australia's is heading for a shortage of rental properties.

He's not wrong.

Population growth has only just begun to increase again, and yet rental vacancies are already notching all-time lows.

We can expect to see record high population growth over the next few years.

But the combination of rising interest rates and APRA's extraordinary 3 percentage points lending assessment buffer is going to effectively cripple the rental supply.

Vacancy rates for units are now at record lows at under 1 per cent, according to CoreLogic.

Source: CoreLogic

Unit rents are now soaring, rising by 13 to 14 per cent annually in the three most populated capital cities.

Source: CoreLogic

I recently noted the global war for talent and the forthcoming Big Australia debate here.

Retail weakening

Retail turnover was down -0.2 per cent in October, and -0.6 per cent excluding food purchases.

James Foster with the graph:

Given retail prices have increased, including for food after recent flooding, this suggests that retail turnover in volume terms is sinking.

And particularly so for household goods and department store retailing.

I used to do detailed analysis of all the figures by sector and state, but it seems superfluous now as other people are doing it better and on a more timely basis!

Alex Joiner from IFM:

Source: Alex Joiner

It's a really big week for economic data, which will serve as a decent litmus test for how much the economy has slowed so far as a result of the tightening of monetary policy.

Given new home sales have collapsed, I would guess that the economy has slowed a bit to date, but that'll be nothing compared to what we see in 2023.

Brexit tensions

A couple of decades ago I lived in the south-east of England (a crowded trade if ever there was one!).

There were theories doing the rounds, even in the pre-Youtube days, that as the Baby Boomer generation moved on the population of the UK would halve, effectively leaving the island half empty.

It never made any logical sense, and in any case it contradicted the evidence of my own eyes, which could see towns and cities sprawling at a very rapid pace, worsening traffic queues, crowded schools and hospitals, and so on.

Between the most recent two Censuses the English population continued to expand rapidly by around 3½ million to more than 53 million.

To state the obvious, that's an awful lot of people - and extra people! - for such a small space.

It's a lot, however you may try to position it, particularly due to the gravitational pull of London and the south-east of England.

A little while ago the Office for National Statistics (ONS) forecast that the England population would grow by a further 3½ per cent over the course of this decade, with the total UK population expanding by 3.2 per cent to 67.1 million by 2030.

Not all that surprisingly this has been causing significant angst in some towns and cities, and the desire to "take back control of the borders" was arguably a key swing factor in the controversial 2016 Brexit referendum, which ultimately voted 52 to 48 in favour of leaving the European Union.

UK hits record immigration

Ironically, despite the government's strong rhetoric, there has been no apparent "taking back control of the borders" to speak of, however loosely that may be defined.

Statistician and social commentator Jamie Jenkins forecasts that more than 50,000 migrants will cross the channel in small boats this calendar year alone.

Approximately half of the migrant crossings are accounted for by Albanians, overwhelmingly male.

Where I stay when in the UK, half a dozen of the town's local hotels are reportedly being used to provide accommodation for the new arrivals while the Home Office processes asylum seeker claims.

These local stories can be beaten up, no question, but the headline numbers and associated costs are real enough.

Yesterday the ONS also reported that the net immigration figures for the year to June 2022, which showed more than 1.1 long-term immigration million arrivals, for a net immigration figure of a staggering +504,000.

Source: ONS

Students accounted for a large part of the surge, taking the net immigration figures into the UK to the highest level on record.

After accounting for the natural growth in the population this clearly implies that the population forecasts for the decade are significantly undercooked.

Global war for talent

Germany and some other European countries have already gone done the mass immigration route, with decidedly mixed results.

Recently Canada announced that it would be targeting a huge immigration programme over the coming years.

This suggests that there could be something of a global 'war for talent' afoot in the years ahead.

Hong Kong has dropped out of the race as its talent pool is drained following the en masse exodus of graduates and skilled workers.

What next for 'Big Australia'?

The Big Australia debate has been tarnished over the years since the mining boom glory years, since anyone daring to question what the 'appropriate' level of immigration might be is immediately tarnished with the xenophobia brush by big business and other vested interests.

But in the context of what's happening in Germany, the UK, Canada, and elsewhere, it's a vitally important debate for the functioning of the country, which merits a fair discussion.

Home Affairs recently announced that Australia had processed 3 million visas since June, reducing the backlog to around ¾ million.

Yesterday, Andrew Giles updated Parliament in noting that 3.4 million visas have now been crunched through since June 1.

That accounts for a big chunk of the backlog, and it's fairly clear what direction things are currently heading in.

But what comes next?

Australia is already likely to see its population increase from 26 million to 29 million by the end of 2030, based on the current trajectory and forecasts.

An inquiry is due to be held over the coming few months into the role of permanent migration and nation building.

The big picture is that if Australia goes down the 'Big Australia' route the population could feasibly increase to around 50 million by 2050, and...who knows, perhaps 100 million by 2100?

Of course, I'm acutely aware as an immigrant that it's not really my debate to get involved in.

But clearly the question which needs to be asked and answered transparently is whether that is the goal, and whether the benefits outweigh the costs?

Ultimately, that's the crux of the entire debate.

Big Picture podcast

I joined Michael Yardney to discuss the prospect of an economic downturn and what it means for property markets.

Tune in here (or click on the image below):

Property Pod

This week I was joined by Melinda Jennison from Streamline to discuss what's happening in Brisbane's housing market, following on from recent headlines.

Tune in here (or click on the image below):

You can also tune in at Apple podcasts, and Spotify.

And also you can listen at Youtube here: