Bond carnage

Lots of excitement in bond markets today, with speculators sensing that the Reserve Bank has abandoned its yield curve control (YCC) targets and sending yields soaring.

This has garnered much international attention and plenty of speculation about whether the YCC regime is set to be ditched next week, with the Reserve Bank of Australia choosing not to step in and buy April 2024 bonds today.

There hasn't been any formal communication from Martin Place, adding to the consternation, so we'll see what next week's meeting brings.

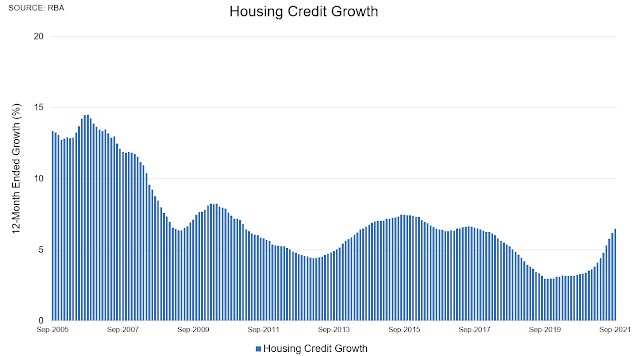

Credit acceleration rolls over

Looking at the historic RBA data released today in relation to financial aggregates, housing credit growth picked up a bit further to 6½ per cent.

Tightening underway

Futures markets are pricing for multiple hikes in the cash rate by the first quarter of calendar year 2023, though I guess I'll only believe that when I see it.

There's little doubt that we'll get a spike in inflation over the coming year, but all of the old deflationary forces have hardly gone away (technological shifts, outsourcing to Asia, declining union membership, the casualisation of the workforce, etc.), and wages growth is still stuck at record low levels.

The prospect of interest rates rising sooner than previously expected will also give rise to the usual incorrect extrapolation about a swathe mortgage defaults, even though major bank data released recently suggests that households are well ahead on repayments and have never had so much buffer sitting in mortgage offset balances.

Rising mortgage rates may negate any moves to implement further macroprudential measures, but new mortgages will now be assessed with an enormous 3 per cent serviceability buffer built in, while there's also ample headroom for any stressed borrowers to shift to more comfortable interest-only terms should a release valve ever be required.

ANZ reported this week that only 9 per cent of its home loan book is now on interest-only terms, which represents an extraordinary decline over recent years.

Rising mortgage rates? Sure. Widespread mortgage defaults? It's a non-starter.