Record migration program

As in many developed countries, Australia's economy has been grappling awkwardly with capacity constraints.

The cavalry will soon be on the way, though!

Visa processing is being fast-tracked, there are now on average some 10,000 student visa applications per week, and the Labor Party - having being essentially silent on population policy plans through the election campaign - is now reportedly looking to ramp up the immigration program to 200,000 per annum.

As the number of temporary visa holders rebounds, it's entirely possible that the growth in resident population could reach or exceed a record high of 500,000 per annum over the next couple of years, after accounting for the natural growth of the population of around 150,000 per annum (i.e. births minus deaths).

For the time being, at least, tens of thousands of Aussies are taking a well-earned break and travelling overseas, but the return of international students appears likely to take some of the pressure off the labour market as we head into the summer months.

Week ahead

There is a huge data dump due out this week, so let's take a quick preview of some of the key releases.

Firstly, while overseas departures are riding fast (increasingly so as the rising number of short-term arrivals begin to cycle back out), we'll start seeing monthly arrivals come surging back to above 1 million over the coming months.

Wages growth is likely to come in at around only 0.7 per cent or 0.8 per cent for the June quarter, perhaps allaying some of the concerns of a 'spiral' in incomes (wages growth is also rebounding from record lows in 2020).

The jobs release is another hugely important and anticipated data series; and looking at jobs vacancies figures it's likely to be another very solid set of numbers.

The unemployment rate is already very low at just 3.5 per cent, after a huge drop last month. Will it fall even further this month? Naturally this could further inform monetary policy if so.

Turning point

The Sydney Morning Herald reported upon a symbolic turning point for the big smoke today, as 60,000 runners showed up for the resurgent City2Surf, while the SCG was a packed house of 44,500 for the Sydney Swans game (the third highest ever AFL crowd at the cricket ground).

Sydney is back, read the headlines!

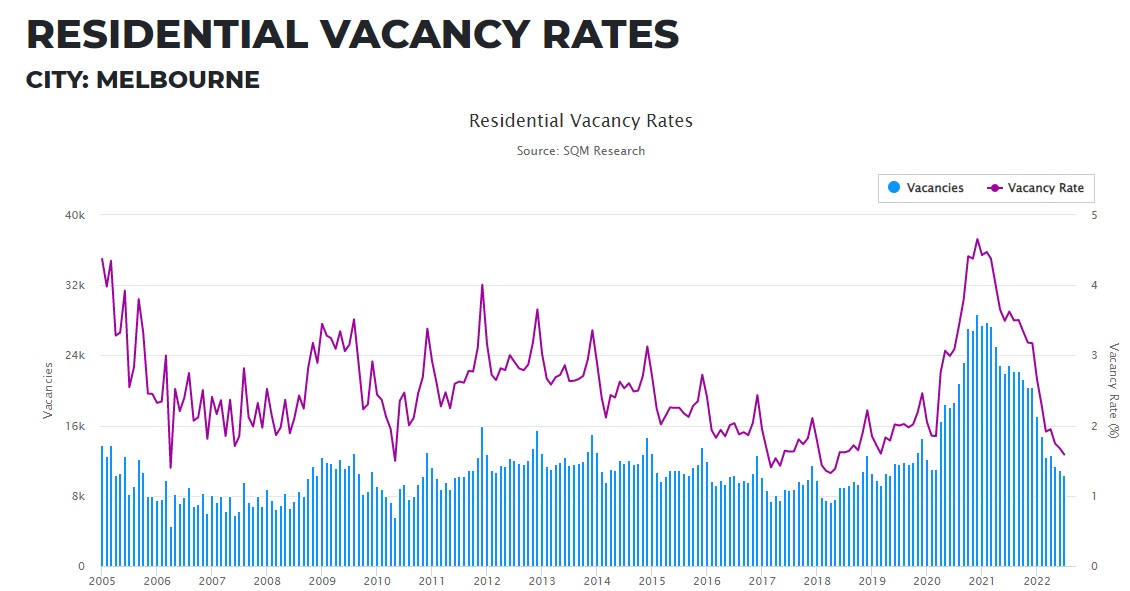

In a similar vein, SQM Research will report a national residential rental vacancy rate of just 1 per cent for July, with rental pressures easing in Adelaide, Hobart, Perth, and Canberra respectively, but with clear signs of a huge rotation back towards Melbourne and Sydney, both of which will record another drop in rental vacancy rates.

Source: SQM Research

Rents are continuing to accelerate across the capital cities, according to CoreLogic's latest figures.

Sentiment shift

There has been some evidence of a sentiment shift in the property market over the past week or two, with rents and now auction clearance rates both rising, immigration about to surge towards record highs, and fixed mortgage rates falling back following some alarming spikes.

Consumers are perhaps starting to believe that the terminal cash rate for this cycle may not be quite as bad as previously feared.

There is a missing piece in the housing market puzzle, though, and that's the massive 3 per cent assessment buffer on new loans, which will be

far too high from next month, and will stymy the ability of landlords to borrow and supply badly needed new rentals.

In fact, plenty of landlords have actually been choosing to offload rental properties due to their ongoing inability to refinance, punitive changes in land tax rules, ever-trickier tenancy and ‘no eviction’ laws, as well as rising mortgage rates and trades/renovation costs.